Welcome to Wealth Wisdom—Your Financial Edge Starts Here

Every issue of Wealth Wisdom is your go-to guide for practical insights, real-world strategies, and a dose of encouragement to help you build lasting financial confidence.

Inside, you’ll find clear tips, expert tools, and inspiring content to simplify your money decisions and move you closer to your goals—whether you’re building from scratch or ready to take things to the next level.

This is more than a newsletter—it’s your momentum.

Let’s grow stronger, smarter, and more financially free—together.

May 2025 Issue 2

May 2025 Issue 2

I wish to have future newsletters sent directly to my inbox when they become available.

Your privacy is important to us. When you share your email, we use it solely to send you helpful wellness content and updates — you can unsubscribe anytime. We will never sell or share your information with anyone, ever.

Welcome to this month’s edition of Wealth Wisdom! Today, we’re diving into one of the most powerful yet overlooked tools for building long-term financial success: budgeting. A smart, realistic budget isn’t about restriction—it’s about direction.

Let’s break it down step-by-step so you can take control of your money and

build a solid foundation for lasting wealth.

Welcome to Issue 2 of Wealth Wisdom!

Budgeting That Works: The Foundation of Wealth

Budgeting That Works: The Foundation of Wealth

Introduction: Why budgeting is the cornerstone of financial health

Step-by-step guide to creating a monthly budget

Apps / Tools to simplify budgeting

Real-life example of someone who gained control through budgeting

Call-to-Action: Download our free budget planner worksheet

Introduction: Why budgeting is the cornerstone of financial health

Introduction: Why budgeting is the cornerstone of financial health

Budgeting is often seen as restrictive, even tedious—but in reality, it’s one of the most empowering habits you can develop for your financial well-being. At its core, a budget isn’t about saying “no” to things—it’s about saying “yes” to what matters most. It gives you a clear roadmap for where your money is going, what it’s doing for you, and how it can align with your short- and long-term goals. Whether you’re saving for a home, paying off debt, planning a vacation, or simply trying to make ends meet, budgeting is the foundation that supports every other financial decision you make.

One of the greatest benefits of budgeting is that it creates clarity. Too often, people find themselves living paycheck to paycheck or wondering why they can’t seem to get ahead—without realizing that a lack of awareness is the root cause. A solid budget gives you visibility into your income, expenses, and spending patterns. Once you know where your money is going, you can make informed decisions and take intentional action. That’s how people begin to shift from reactive to proactive financial living.

Budgeting also builds discipline—and discipline creates freedom. When you budget effectively, you’re no longer guessing at your bank balance, scrambling to cover surprise expenses, or feeling guilty after making impulse purchases. Instead, you’re confidently setting aside money for the essentials, for enjoyment, and for the future. That might mean creating an emergency fund, investing in retirement, or finally taking that family trip you’ve dreamed about—all without going into debt or sacrificing your peace of mind.

Another reason budgeting is foundational is that it enables you to prioritize your values. Your budget becomes a reflection of what’s most important to you. Want to give more generously? Travel more frequently? Reduce financial stress at home? All of that starts with a plan for your money. Without one, your financial life becomes a series of unplanned expenses and missed opportunities.

Lastly, budgeting is scalable. It doesn’t matter if you’re earning $30,000 a year or $300,000—if you don’t manage your money with intention, you’ll struggle. But when you learn to budget at any income level, you set the stage for long-term growth and success. It’s not about how much you make—it’s about how well you manage what you have. In the end, budgeting is less about restriction and more about alignment. It’s about aligning your income with your goals, your habits with your values, and your future with your decisions today. That’s why budgeting isn’t just a good idea—it’s the cornerstone of financial health.

Step-by-step guide to creating

a monthly budget

Step-by-step guide to creating

a monthly budget

1. Calculate Your Total Monthly Income

Include all sources: salary, freelance work, Social Security, pensions, rental income, etc.

Use net (after-tax) income for the most accurate picture of what you can spend.

2. List All of Your Monthly Expenses

Start with fixed expenses (same amount every month): rent/mortgage, insurance, loan payments, subscriptions.

Then list variable expenses (change month to month): groceries, gas, dining out, entertainment, etc.

3. Categorize Your Spending

Group expenses into categories like housing, transportation, food, personal care, and savings.

This helps you identify which areas might be consuming more of your budget than necessary.

4. Set Spending Limits for Each Category

Use your past few months of bank statements or receipts to estimate what’s typical.

Adjust amounts to fit your income and ensure you’re not overspending.

5. Include Savings, Tithing, and Debt Repayment as “Non-Negotiables”

Pay yourself first! Prioritize building an emergency fund, saving for retirement, or paying down high-interest debt.

Allocate specific dollar amounts for each savings goal and debt payment.

6. Use the 50/30/20 Rule as a Guideline (Optional)

50% for needs (housing, utilities, food)

30% for wants (dining out, hobbies, entertainment)

20% for savings and debt repayment

Adjust as needed based on your personal situation.

7. Track Your Spending Throughout the Month

Use a budgeting app, spreadsheet, or journal to log expenses regularly.

This keeps you accountable and helps you spot problem areas before they grow.

8. Review and Adjust at Month-End

Compare your actual spending to your budget.

Note where you went over or under, and adjust categories for next month accordingly.

Celebrate small wins and progress—it’s about improvement, not perfection!

9. Make It a Habit

Set a recurring calendar reminder to revisit your budget at the end or beginning of each month.

The more consistent you are, the more in control and empowered you’ll feel.

With these steps, your budget becomes more than a spreadsheet—it becomes a tool for building the financial future you truly want.

Apps / Tools to simplify budgeting

Apps / Tools to simplify budgeting

In today’s fast-paced world, managing money can feel overwhelming—but thanks to modern technology, budgeting has never been easier. Apps and digital tools take the guesswork out of tracking income and expenses, making it simpler and more convenient to stay on top of your finances. Whether you’re a seasoned saver or just starting out, the right tools can turn budgeting from a chore into a consistent and rewarding habit.

One of the biggest advantages of using budgeting apps is automation. Instead of manually writing down every transaction, these tools link to your bank accounts and credit cards, automatically categorizing spending and providing a real-time snapshot of where your money is going. This helps you spot patterns, curb overspending, and stay aligned with your financial goals.

Another benefit is accessibility. With mobile apps, you can check your budget anywhere—whether you’re grocery shopping, paying a bill, or planning a vacation. Instant access keeps you informed and accountable, reducing the chances of impulse buys or overlooked expenses.

Budgeting tools also offer customization and goal setting. You can create categories that reflect your personal lifestyle and priorities, set savings goals, and even receive alerts when you’re nearing a spending limit.

Here are a few popular budgeting tools worth exploring:

You Need A Budget (YNAB) – A powerful app focused on proactive money management, giving every dollar a job. Great for goal setting and building long-term habits.

Mint – A user-friendly, free app that tracks all your accounts in one place, categorizes expenses automatically, and provides spending insights. EveryDollar – Created by Dave Ramsey’s team, this zero-based budgeting tool helps you assign every dollar of income to a specific purpose. PocketGuard – Helps you understand how much you have left “in your pocket” after essentials and bills are accounted for.

By taking advantage of these tools, budgeting becomes less about stress and more about strategy. The easier it is to stay organized, the more likely you are to stay consistent—and consistency is what leads to real financial freedom.

Real-life example of someone who gained control through budgeting

Real-life example of someone who gained control through budgeting

Real-Life Story: How Budgeting Helped the Taylors Take Back Their Financial Future

Just over a year ago, Mark and Lisa Taylor sat at their kitchen table, surrounded by a pile of unopened bills and bank statements. Both in their early 50s, they had steady incomes—Mark worked in sales, and Lisa was a school administrator—but despite earning decent money, they felt like they were always treading water financially.

“We honestly had no idea where our money was going,” Lisa shared. “We weren’t living lavishly, but somehow we were always coming up short by the end of the month. It felt like we were stuck in a loop—working hard, paying bills, and still falling behind.”

The breaking point came when they realized their credit card balances had quietly crept up to over $18,000. Car payments, home improvements, a couple of unplanned expenses—they had all added up. When they calculated the interest they were paying each month, they were stunned. “We weren’t just living paycheck to paycheck,” Mark said. “We were sinking.”

That’s when they decided to make a change.

Lisa came across a budgeting workshop online and convinced Mark to go all-in with her. They sat down together and created their very first written monthly budget. For the first time, they tracked every dollar—income, bills, groceries, gas, even their Friday night takeout.

They also adopted the debt snowball method—listing their debts from smallest to largest and attacking the smallest one first while paying minimums on the rest. Each time they knocked one out, they rolled that payment into the next one. With every success, their confidence grew.

“It wasn’t easy at first,” Mark admitted. “But seeing those balances go down was addictive. We started cooking more at home, trimmed our subscriptions, and sold a few things we didn’t need.”

Within just 12 months, they had paid off all of their consumer debt. “We never imagined we could do that so quickly,” Lisa said. “The budget gave us direction. The debt snowball gave us momentum.”

Today, the Taylors still sit down every month to plan their budget—only now, they’re setting goals for travel and retirement instead of playing catch-up. “Budgeting didn’t restrict us—it freed us,” they say. “And we’re never going back.”

Call-to-Action: Download our free budget planner worksheet

Call-to-Action: Download our free budget planner worksheet

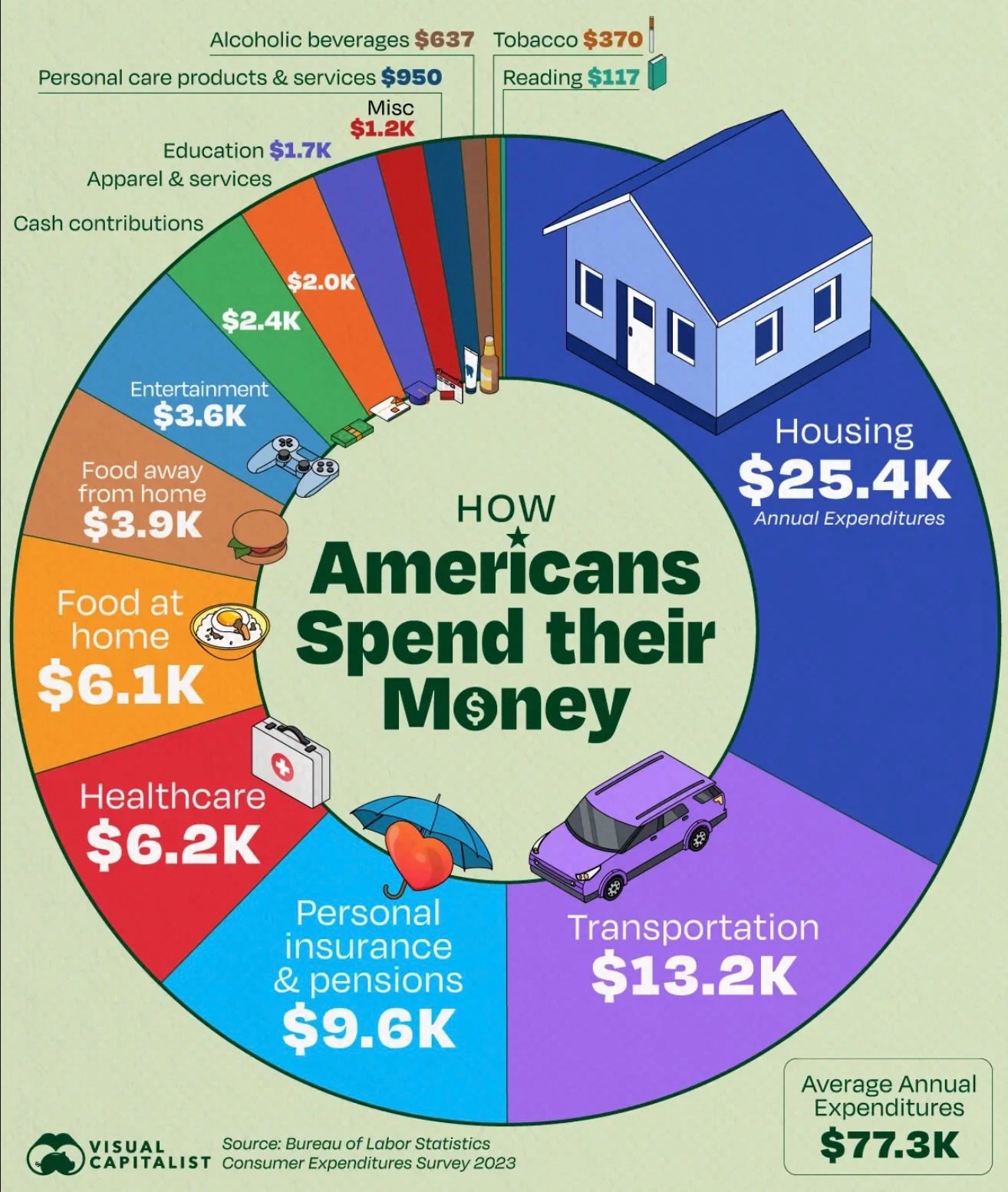

Creating a solid budget means accounting for every dollar and giving it a purpose. A well-rounded budget isn’t just about the big-ticket bills—it’s about building a realistic picture of your lifestyle so you can manage money effectively, avoid overspending, and plan for the future. Below is a breakdown of essential budget categories you should include, no matter your income level.

1. Housing

This is usually your largest monthly expense and includes rent or mortgage payments, property taxes, homeowner’s or renter’s insurance, and utilities like electricity, gas, water, and internet. Experts suggest keeping this category under 30% of your monthly income.

2. Transportation

This includes car payments, insurance, fuel, maintenance, and public transportation costs. Don’t forget to include tolls, parking fees, or rideshare apps like Uber or Lyft if you use them regularly.

3. Personal Insurance and Pensions

Contributions to retirement accounts (like 401(k), IRAs, or pensions) and life insurance premiums belong here. If these aren’t automatically deducted from your paycheck, it’s crucial to include them in your budget.

4. Health Care

Out-of-pocket expenses like health insurance premiums, doctor visits, prescription medications, dental care, and vision services should be included. Even if you’re healthy, it’s wise to budget for occasional or emergency health costs.

5. Food at Home

This category includes your grocery bill—anything you buy to prepare meals at home. Track what you typically spend and look for areas to cut waste without sacrificing nutrition.

6. Food Away from Home

Dining out, coffee runs, fast food, and takeout fall into this category. It’s often a surprise expense that adds up quickly. Set a realistic cap and track it closely.

7. Entertainment

Budget for leisure activities like movies, concerts, streaming services, sports, hobbies, and vacations. Having fun should be part of a healthy budget—but only when planned in advance.

8. Cash Contributions

This includes charitable donations, church giving, tithes, or monetary gifts to friends and family. If you’re a regular giver, plan it into your budget just like any other expense.

9. Apparel and Services

This includes clothing, shoes, dry cleaning, tailoring, and other garment-related services. Consider a seasonal clothing allowance rather than impulsive purchases.

10. Education

Tuition, books, supplies, online courses, and student loan payments belong here. If you’re saving for your child’s education, include contributions to a 529 plan or other savings vehicle.

11. Personal Care Products and Services

Include haircuts, skincare products, cosmetics, toiletries, and salon visits. While not usually large, these add up over time and should be tracked.

12. Alcoholic Beverages

Whether you enjoy the occasional glass of wine or host social gatherings, include this category if it’s part of your lifestyle. Keeping it separate helps maintain an honest look at discretionary spending.

13. Tobacco

If applicable, account for cigarettes, vaping products, or other tobacco-related purchases. It’s a personal expense that should be tracked to manage spending and explore potential areas to cut back.

14. Reading Materials

Books, magazines, newspapers, or digital subscriptions such as Kindle Unlimited or Audible fall into this category. These can be educational or recreational, but either way, they deserve a line in your budget.

Conclusion

A comprehensive budget accounts for both needs and wants. By organizing your finances into clear categories like these, you gain insight, control, and the power to make intentional decisions. Budgeting isn’t about restriction—it’s about creating a plan that reflects your values and builds a strong financial future.

Congratulations on taking a meaningful step toward financial freedom! This budgeting worksheet is more than just a spreadsheet—it’s your personal roadmap to a clearer, more confident financial future. Whether you’re trying to get out of debt, save for a goal, or simply understand where your money is going, this tool will help you take control and make intentional, informed decisions.

Many people think budgeting is about restriction, but in truth, it’s about freedom. When you create a budget, you’re telling your money where to go instead of wondering where it went. A budget gives you visibility, purpose, and peace of mind. And best of all—it works for every income level and life stage. If you can add, subtract, and be honest about your spending, you can build a successful budget.

This worksheet is a tool for empowerment. Whether you print it out, use it digitally, or rewrite it every month, make it your own. Be honest, stay consistent, and remember—a budget is not about perfection, it’s about progress.

You’re not just filling in numbers—you’re building a better financial future. Let’s get started!

Budgeting Worksheet from Consumer.gov

As part of your journey toward financial clarity and control, we recommend this trusted tool provided by Consumer.gov, a website managed by the Federal Trade Commission (FTC). It offers a simple and effective budgeting worksheet that’s perfect for beginners and seasoned planners alike.

This downloadable PDF can help you organize your income and expenses, set spending limits, and track progress over time.

It’s a great complement to our West Egg tools and provides another step forward in taking control of your money.

Bonus Material

Bonus Material

In a recent blog from 2024, I took a deeper dive into the power of budgeting and how it can truly transform your financial future. From practical tips to mindset shifts, it’s a must watch video for anyone ready to take control of their money. You can check it out and watch the full video by clicking the play button on the left.

If you’re new to West Egg Wealth, be sure to click on our Getting Started icon. There, you’ll find downloadable materials, free guides, and practical tools designed to help you build stronger financial habits and gain confidence with your money. It’s the perfect place to begin moving toward better financial health and long-term stability.

If you have any questions, thoughts, or comments you'd like to share, I'm always happy to hear from you - just send a message to info@westeggliving.com

I'm here to help!

Thank you for joining us for this edition of Wealth Wisdom! We hope you found valuable insights and encouragement as you take steps toward a stronger financial future. It’s an honor to walk alongside you as you grow in financial knowledge, confidence, and peace of mind. Remember, you’re not alone on this journey—and we’re here to support you every step of the way.

Stay tuned for next week’s issue packed with more tips, insights, and motivation. Until then, be kind to yourself and keep moving forward — you’ve got this!

The content provided on this West Egg Wealth is for informational and educational purposes only and should not be considered financial, legal, or professional advice. Always consult with a qualified professional before making any changes to your personal finances. Individual results may vary and West Egg Wealth makes no guarantees regarding specific outcomes.

Use of this website and associated materials constitutes acceptance of our

I love the video on this one.

I will try dinking water every hourr like I am trying to go 250 steps each hour.. Encouraging idea.

This is great information. I love the new layout. I cannot wait for the next edition!!!

Thanks Riaan.

Great article!